Strategic Importance of US Dollar

The global debt market, estimated at approximately US$315 trillion, is fundamentally anchored by the US Dollar, which dominates 60% of global debt issuances. Additionally, the US Dollar accounts for nearly 89% of all foreign currency trades, 58% of global foreign exchange reserves, and almost half of SWIFT payments and cross-border loans. This dominance ensures superior liquidity and depth across investment-grade, high-yield, and emerging market credits, making the US Dollar a cornerstone for global portfolios.

US Dollar: Market Depth & Liquidity

Representing approximately 70% of global corporate bonds, the US dollar bonds offers unmatched depth across Investment Grade, High Yield, and Emerging Market segments. This liquidity supports tighter bid-ask spreads, better price discovery, and smoother entry and exit points—especially vital during periods of market volatility.

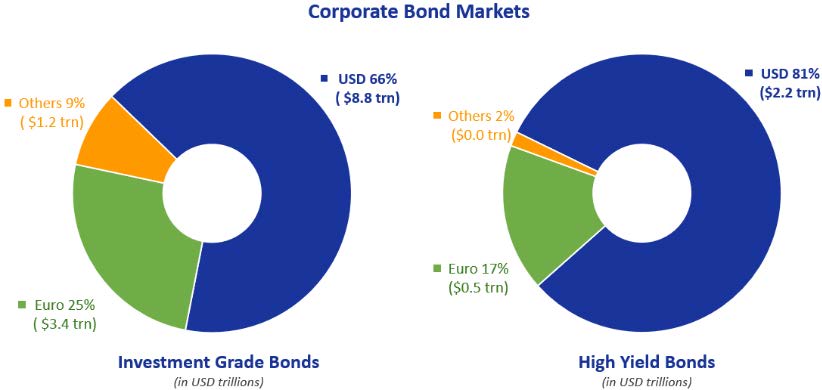

Comparison of Euro Bonds against US Dollar Bonds

Euro Market Size

While the Euro corporate bond market is substantial, it remains only one-third the size of the US dollar corporate bond market, as follows:

USD Corporate Bonds Outstanding: $13 trillion

EUR Corporate Bonds Outstanding: $4 trillion

Euro Market Width and Depth for EM Issuers

For Indian and other emerging market issuers, the USD bond market offers broader access, enabling greater portfolio diversification and more targeted credit exposure, as seen below:

Indian Issuers in USD: Over 110 bonds totaling over $60 billion

Indian Issuers in EUR: Just 2 EUR bonds totaling €800 million.

USD Bonds Yield Premium over Euro

USD bonds offer a substantial yield premium, enhancing overall portfolio returns without necessarily increasing credit risk, as follow:

Investment Grade Yield: USD 4.90% versus EUR 3.30%

High Yield: USD 7.00% versus EUR 5.80%

Structural Limitations of Euro Bond Market

The EUR corporate bond market remains fragmented, predominantly driven by issuances from France and the Netherlands.

Non-financial corporate issuances in the Euro area stands around €1.7 trillion (Q2 2024), with banks still being the primary source of corporate credit.

Liquidity remains constrained with notably lower repo and secondary market activities compared to the US dollar liquidity.

The investor base is heavily concentrated, with approximately 50% of bonds held within the euro area and only around 20% by non-EU investors.

The European System of Central Banks (ESCB) holds approximately 13% of outstanding euro corporate debt, with planned reductions of just €20 billion by mid-2025.

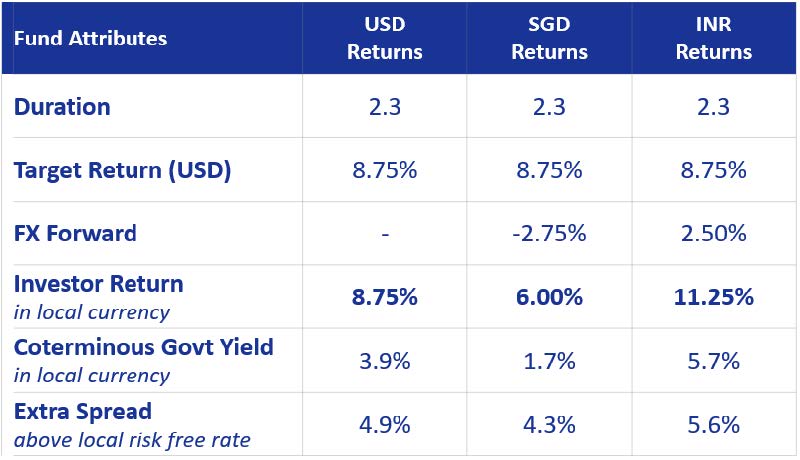

Dollar Returns in Local Currency

Investors can hedge USD exposure into local currencies to access deeper markets, control FX risk, and enhance returns while maintaining base currency exposure.

For example, a 3 to 4 years fixed maturity enhanced returns US dollar bond fund could deliver:

In US Dollars: 8% - 9% per annum

In SGD-hedged class: 6%-7% per annum

In INR-hedged class: 10%-12% per annum

These returns significantly outperform respective risk-free treasury rates, offering compelling value for local currency investors, as follows:

Verifying access...