This articled originally appeared on YielReport as a 2-part article: “Is Turkey a Turkey? Perceptions of an Investment Manager (Part I)” and “Is Turkey a Turkey? Perceptions of an Investment Manager (Part II)” written by guest contributor Sanjay Guglani, CIO, Silverdale Fund Management.

Part I

The first part of this article expounded the situation in Turkey and its genesis.

While it is not known why release of a pastor became a key point for the president of the United States, what is indeed known is that an estimated 80% of evangelist Americans had voted for Trump in the 2016 presidential election. Interestingly, the US has refused to deport Fethullah Gulen, a Turkish cleric living in Pennsylvania, who is accused of plotting the 2016 attempted coup against Erdogan. On August 10, 2018, Trump decided Turkey’s export of steel and aluminium to the USA to be a national security threat and he announced a doubling of tariffs thereon via Twitter. In the context of a strengthening US dollar and rising oil prices (Turkey is a net importer of oil), the tariff increases led to a massive depreciation of the Turkish lira, dragging with it other emerging economies’ currencies.

Why Turkey’s currency crisis could be fatal

The key risk is that the currency crisis could become a debt crisis. At an exchange rate of 1 US dollar to 6 Turkish lira, a USD 100 debt is equal to TRY 600. However, if the Turkish lira depreciates, such that 1 USD is equal to 11 Turkish Liras, the same debt balloons to TRY 1,100. Such a depreciation leads to a larger effective debt as well as making debt servicing more onerous. This could become a vicious circle of spiralling debt, massive failures, bankruptcies and contagion.

How is high inflation tamed?

The basic tenets of economics demand that in case of rapid inflation (especially when the economy is growing at a supra-optimal rate of 7.4% (Q1, 2018) with a high current account deficit (at 6.5% of GDP), the central bank of the country should raise interest rates. By increasing interest rates, affordability of loans drops, hence there is less money in the economy. Since there is less money to fuel demand for goods and services, prices fall. That is, inflation falls.

What’s at root of Turkey’s problem?

Turkey’s President Erdogan believes that high interest rates cause inflation and hence he is against increasing interest rates. He has repeatedly proclaimed that high interest rates are the mother and father of all economic evils and he has asserted “no surrender on interest rates as long as I’m alive”.

The current situation is precarious because Erdogan won elections because of his opposition to high interest rates. In 2001, a rapid flare-up of inflation led to a massive depreciation of (old) Turkish lira (TRL) by over 60%. As Turkey’s government ran out of foreign exchange to pay for imports and other credit obligations, it had to be bailed out by the International Monetary Fund (IMF). As a precondition of the bail-out, the IMF required Turkey to undertake various financial sector reforms, including increasing the then-prevailing interest rate, thus reducing demand in order to tame inflation. As a side effect, Turkey’s economic growth rate slowed.

All adversities provide opportunities to a shrewd politician and Erdogan was no exception. He seized on the opportunity and won the presidential election promising a reversal of austerity measures, which by then had served their purpose and needed to be lifted. The 2008 global financial crisis and subsequent quantitative easing lowered global interest rates, further aiding Erdogan’s plans of lower interest rates. This massive monetary policy stimulus led to rapid growth of Turkey’s economy, finally pushing it to higher than sustainable growth rates. The reversal of global interest rates has turned the tables for Turkey.

On the political front, in July 2018, Erdogan changed the constitution of Turkey to consolidate power in the hands of the president. On being re-elected under the new constitution, he removed Deputy Prime Minister, Mehmet Simseka, a former economist at Merrill Lynch, and made his son-in-law, Berat Albayrak, finance minister. Now, despite surging inflation and a deteriorating current account balance, the central bank is not increasing its interest rates, which in turn is causing a rapidly-falling Turkish lira. The central bank policy rate of 17.75%, a one-week repo rate, has been held constant since 24 July 2018.

Turkey has a relatively-low foreign exchange reserve of US$80 billion, which is less than 10% of its GDP. Its total external debt is USD$466.7 billion (53% of GDP as of March 2018), out of which USD$118 billion is maturing within a year. Also, Turkey’s non-financial companies’ non-lira liabilities are US$337 billion (May 2018) as against non-lira assets of US$120 billion, resulting in a currency mismatch of US$220 billion. The soft underbelly of Turkey is its high current account deficit of US$57.4 billion, which is 6.5% of its GDP as of June 2018, which is sharply higher than its 2016 value of 3.75%.

Every 10% depreciation of the lira reduces banks’ capital by circa 0.50%, reducing banks’ capital-adequacy reserves and creating the conditions for a recession in Turkey next year.

Part II

The next article will dwell on what capital markets expect from Turkey against what has been done by Turkey. It will address the issues of capital controls and contagion.

What do capital markets expect from Turkey?

At the core of Turkey crisis is the free fall of Turkish lira in the absence of a credible monetary policy. The markets need to see the breaking of the vicious cycle of rising inflation and weakening lira through a sharp increase in interest rates (to slow lending, cool down demand, reduce imports, thus reduce the current account deficit) and assurances from the central bank of its intention to honour debt commitments with no capital controls.

What has Turkey done?

In mid-August, the Turkish central bank (CBRT) lowered its reserve requirement, releasing $10 billion of funding. It has also reduced local liquidity (by not offering one-week repos), forcing banks to either borrow at an expensive overnight rate of 19.25% or to convert dollars into lira. FX swaps have been limited to 25% of banks’ equity (previously 50%), which has severely curtailed borrowing and shorting of lira more difficult. Hence, it provided a temporary respite. Furthermore, most local banks have raised interest rates to circa 25% to stem outflows of deposits (the central bank provides an interest rate floor but it does not provide an interest rate ceiling).

Finally, on 13th September, the central bank increased the interest rate by 6.25%, way beyond market expectation of a 5% hike, thus stemming the currency rout. Erdogan also made it compulsory to trade domestically in Turkish lira, forcing many US dollar-denominated property rentals, car rentals, etc. to be renegotiated and redenominated. This forces residents to convert their US dollars into Turkish lira, indirectly boosting FX reserves. Turkey residents are estimated to have $86 billion of US dollar deposits.

Today (18th September), the CBRT increased its reserve requirement on lira-denominated reserves from 7% to 13%. Its action will lower the availability of money in the economy; hence there will be less money chasing goods, resulting in lower demand, cumulating in a general fall in prices (inflation).

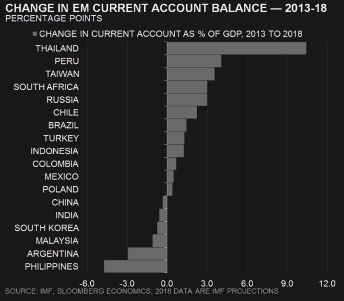

Is there a risk of contagion spreading to other economies?

It seems highly unlikely given the significant improvement in current account balances of emerging economies.

Unlike previous crises, most emerging markets now have flexible exchange rates and they do not need to deplete their foreign-exchange reserves to defend their currencies. Since Turkey’s weight on the MSCI Emerging Markets Index is less than 1%, it would not lead to any significant index-related rebalancing of investments. Even the Eurozone’s exports to Turkey account for less than 0.6% of its GDP.

Importantly, EU banks’ Turkish loan exposure of $224 billion is primarily through subsidiaries of EU banks in Turkey, which are funded in Turkey, with very limited net inbound lending exposure. The key exposures of European banks being:

Spain: BBVA (through Garanti Bank) lending $62 billion, about 15% of the group

France: BNP (through TEB) lending $17 billion, about 2% of the group

Italy: UniCredit (through Yapi), market value of stake $1 billion

Qatar: QNB (through QNB Finansbank) lending $23 billion, about 15% of the group

(Source: BIS, Mizuho)

Could imposition of capital controls help Turkey?

It is very unlikely, because Turkey is not an insular economy. Imports constitute 28% of its GDP and exports constitute 20% of GDP. That is the key reason why Turkey avoided capital controls during the previous crises in 2001 and 2014.

This time too, Erdogan has reiterated several times that capital controls are ‘ruled out’. However, in the absence of wise counsel, if Turkey does impose capital controls, it should be noted that capital controls are ‘controls’ on capital movement and do not constitute a ‘default’; they imply rationing of foreign exchange, making foreign exchange available only for essential imports while curbing remittance of foreign exchange for non-essentials things such as import of luxury goods.

Should Turkey choose to default on its foreign currency debt obligations, it would provide short-term solace. However, it would shut-off Turkish exports, destroy the banking system, curtail foreign direct investments and ruin the country for next 15-20 years. In 2001, even in face of an over-60% depreciation of the old Turkish lira (TRL), Turkey did not impose capital controls. (As an aside, in 2014, Russia did not invoke capital controls despite US sanctions.)

What should investors do?

Investors with exposure to Turkish lira assets may consider reducing their exposures, while those holding Turkish hard currency assets should consider increasing diversification, sticking to high quality assets and reducing duration.

In general, it is important to accept that higher volatility is here to stay. Investors should get used to repeated bouts of volatility spikes. The situation is likely to be aggravated due to increasing dominance of passive investing, reduced market-making (liquidity) provided by banks, central banks sponging-up liquidity in bonds, rising jingoism, etc. Hence, it is advisable to stick to high quality (investment-grade) assets and keep duration low.